As 2026 begins, Real Estate Investment Trusts across Asia are winning back both institutional and retail investors. After several years of rising interest rates, falling valuations and cautious capital flows, listed real estate has entered a recovery phase. This shift shows up in performance, trading liquidity, investor participation and the changing mix of assets within REIT portfolios.

Japan, Singapore and the Philippines show this transition from different starting points. Together, they reveal how stabilising monetary policy and demand for property types with long-term structural support are changing Asia’s REIT markets.

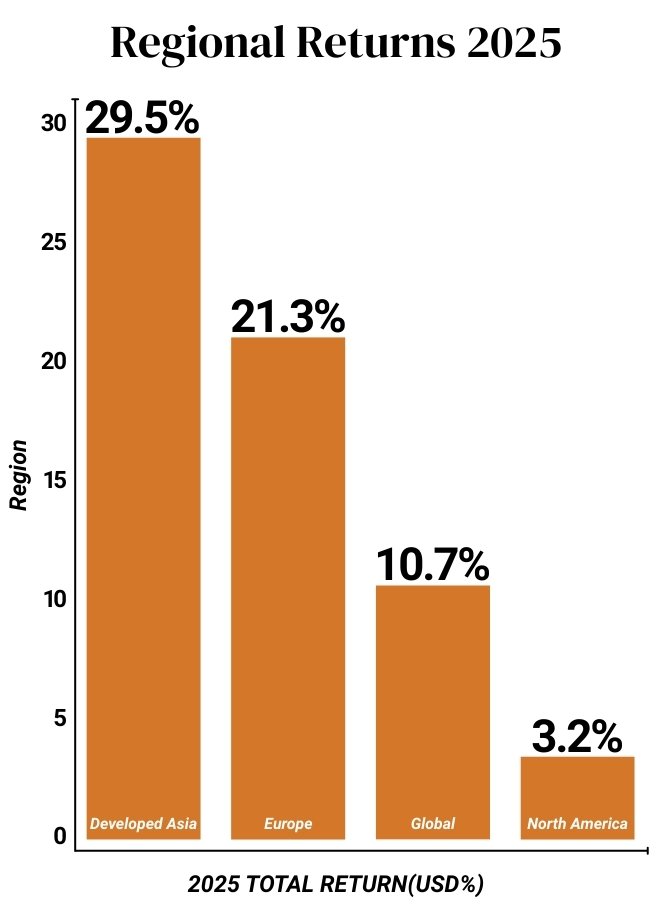

Strong Returns Signal Real Recovery

Asian REITs delivered one of the strongest regional performances globally in 2025. According to FTSE EPRA Nareit data reported in January 2026, the FTSE EPRA Nareit Developed Asia Index recorded total returns of 29.5 per cent in US dollar terms during the year. This beat North America’s returns of 3.2 per cent and outperformed the global Developed Index, which rose 10.7 per cent as higher financing costs continued to weigh on valuations in some markets.

The rebound spread across sectors. Retail, office, diversified and alternative segments all posted strong gains, showing better investor confidence and steadier property market conditions rather than a narrow rally in one specific sector. Performance remained strong in local currency terms as well. Japanese REITs gained around 29.1 per cent in yen during 2025, indicating that the recovery came from asset fundamentals and income visibility rather than currency movements alone.

By early 2026, refinancing risk across major Asian REIT markets had eased. Gearing levels remained largely stable while interest coverage ratios improved as borrowing costs peaked and policy rates levelled out. This provided a more predictable base for distributions and selective acquisitions.

Japan Leads with Diverse and Liquid Market

Japan remains Asia’s largest and most liquid REIT market. The J-REIT universe spans dozens of listed trusts covering office, retail, logistics, residential and alternative sectors. It draws on a broad domestic investor base and operates within a well-established regulatory framework. Market capitalisation stands in the high-teens trillion yen range, making Japan the backbone of regional listed real estate.

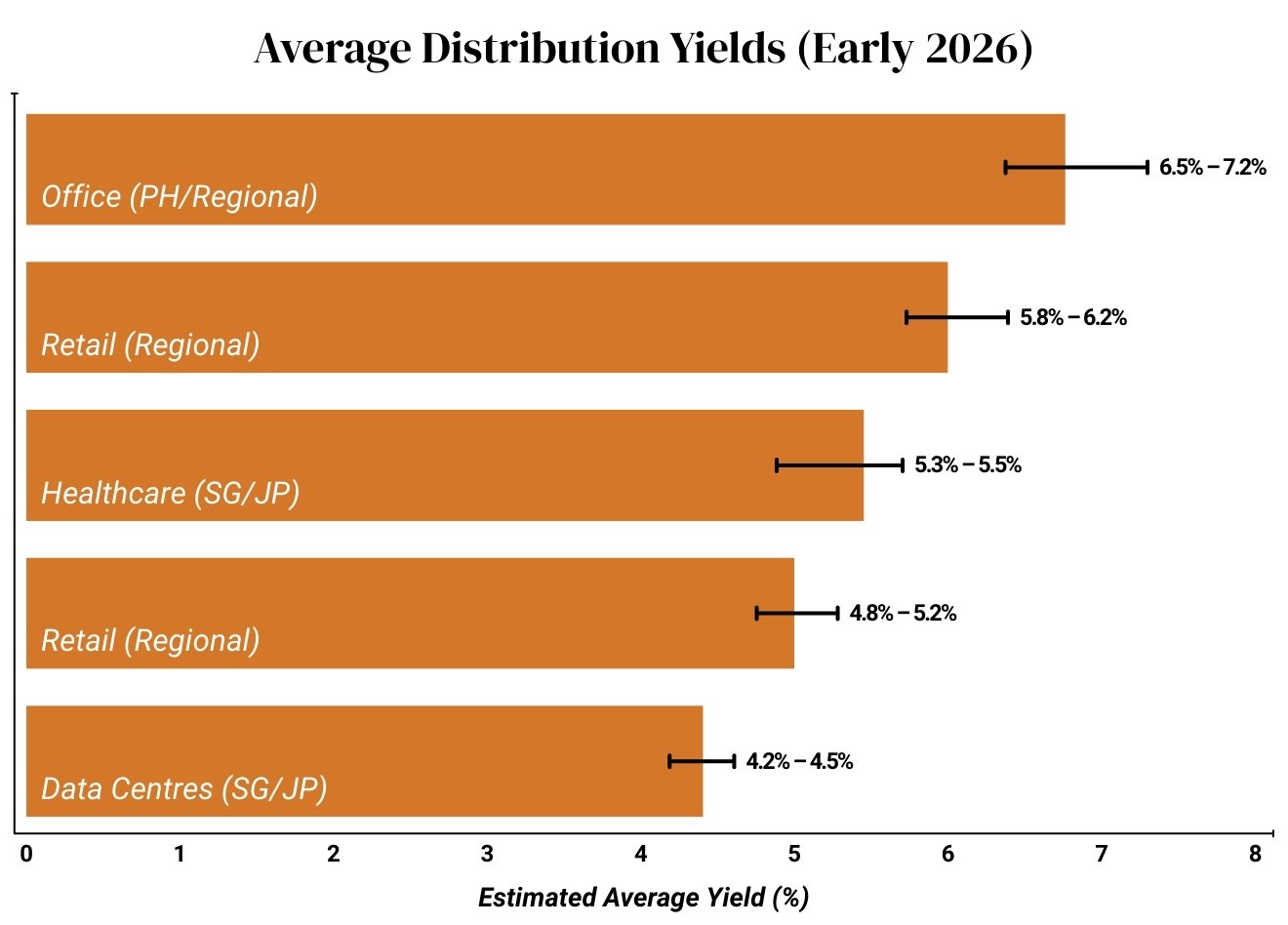

Operating conditions have been steady. In Tokyo, office vacancy in the central five wards tightened to below 2 per cent by late 2025, while overall vacancy across key areas remained low. Logistics, residential and alternative assets recorded even stronger occupancy levels, reflecting structural demand from e-commerce, urbanisation and demographic change. Entering 2026, typical J-REIT distribution yields ranged between roughly 4 and 5 per cent, remaining healthy relative to Japanese government bonds even after the Bank of Japan raised its policy rate to 0.75 per cent in December 2025, its highest level since 1995.

Individual trusts show how the sector is changing. Nippon Prologis REIT, which focuses on modern logistics facilities, maintained occupancy close to 99 per cent through its 2025 reporting periods, supported by e-commerce growth and supply chain changes. Rental income remained stable, and the trust is among those introducing inflation-indexed rent reviews linked to CPI. This marks a notable departure from Japan’s long-standing practice of fixed rents and gives investors greater confidence in the income outlook for logistics assets.

Beyond logistics, Japanese REITs have increased exposure to healthcare facilities, urban mixed-use developments and diversified portfolios. This has reduced reliance on traditional office income and added stability to cash flows at a time when occupier preferences continue to shift.

Singapore REITs Regain Momentum

Singapore plays a central role in Asia’s REIT sector. It ranks among the world’s largest REIT centres by market capitalisation and hosts a wide range of listed trusts holding assets across Asia-Pacific, Europe and the United States. The market benefits from strong governance standards, an experienced investor base and a supportive regulatory framework.

After a difficult period in 2023 and early 2024, Singapore REITs recovered steadily through 2025. The iEdge S-REIT Leaders Index posted total returns around 14.7 per cent for the year as of early December 2025. By early 2026, average distribution yields generally remained in the 5 to 6 per cent range depending on asset type, though premium growth assets such as Keppel DC REIT traded at lower yields of around 4.5 per cent, reflecting their stronger DPU growth profiles. A significant contributor to this recovery was the decline in the three-month SORA, Singapore’s key interest rate benchmark, which fell from around 3 per cent at the start of 2025 to approximately 1.19 per cent by early 2026, directly lowering financing costs across the sector. Balance sheets across leading S-REITs remained conservative, with average gearing in the 35 to 38 per cent range, well below the regulatory limit of 50 per cent.

Data centres have become one of the most visible growth themes. Keppel DC REIT, among the region’s largest pure-play data centre trusts, continued to expand its portfolio across Asia-Pacific and other global markets. In 2025, it reported gross revenue up 42.2 per cent year-on-year to S$441.4 million and distributable income up 55.2 per cent to S$268.1 million. The REIT achieved a record distribution per unit of 10.381 cents, up 9.8 per cent from the previous year, and posted a portfolio rental reversion of 45 per cent for FY2025, driven by renewals of major colocation contracts and highlighting the pricing power these assets carry in an AI-driven market. Portfolio occupancy stood at 95.8 per cent as of late 2025.

Healthcare assets have also become more important. Parkway Life REIT, which focuses on hospitals and medical facilities in Singapore and Japan, achieved a full-year 2025 DPU of 15.29 cents, up 2.5 per cent year-on-year, marking continuous DPU growth since its IPO. Its portfolio is largely supported by long-term master leases, and minimum rents for its three Singapore hospitals are set to rise 24.3 per cent to S$99.1 million in FY2026 under its renewed CPI-linked master lease, providing a clear step-up in income visibility for the year ahead.

Regulatory adjustments in Singapore, including changes to borrowing and capital management rules, have allowed REIT managers to pursue selective acquisitions while maintaining balance sheet discipline. This confidence showed up in fundraising activity, with at least 10 S-REITs raising roughly S$4 billion through equity fund-raising in 2025, the highest level since 2021, to finance new acquisitions. This has supported market liquidity without materially increasing risk.

Philippine Market Offers High Yields

The Philippine REIT market remains relatively small but its relevance continues to grow. Since the introduction of the REIT framework, several office-focused trusts have listed, backed by assets serving multinational firms and business process outsourcing tenants. The broader office market has returned to pre-pandemic behaviour, with Metro Manila recording a post-pandemic high of 847,000 sqm in transactions in 2025, a 13 per cent increase year-on-year according to Colliers Philippines.

During 2025, Philippine REITs offered comparatively high distribution yields, ranging from around 5.5 per cent for benchmark names like AREIT to over 7 per cent for more office-concentrated trusts. This made them some of the higher-yielding options in Asia and supported participation from retail investors seeking alternatives to bank deposits and government bonds.

AREIT, the country’s first listed REIT, expanded its asset base through 2025 by adding logistics, industrial and mixed-use properties alongside its core office portfolio. In the first nine months of 2025, the company posted total revenues of P9.5 billion and EBITDA of P7.0 billion, up 34 per cent and 37 per cent year-on-year. Total assets under management reached P138.9 billion by September 2025, with further infusions expected to push this toward P158 billion. The company maintained high occupancy (99 per cent as of September 2025) and consistent dividend payouts, reinforcing its position as a benchmark for the local market.

RL Commercial REIT has undergone a significant portfolio shift, with 21 of its 38 assets now comprising malls following a series of property infusions from its sponsor Robinsons Land. The nine malls added in 2025 contributed roughly 15 per cent of full-year revenue, reducing reliance on office income and aligning the portfolio with consumer spending recovery trends. The company reported full-year 2025 revenues of P11.08 billion, up 35 per cent from 2024, with portfolio occupancy at 96 per cent. Its inclusion in the PSEi in February 2026 provided a concrete boost to trading activity, placing it among the most liquid and well-capitalised firms on the local bourse.

Data Centres and Healthcare Reshape Portfolios

Across Asia, changes in portfolio composition reflect a broader shift in investor priorities. Traditional retail malls and conventional offices no longer dominate new investment. More capital is now going towards assets with long-term structural demand behind them.

Data centres represent the fastest-growing segment. Asia-Pacific remains undersupplied relative to global digital infrastructure needs, driven by cloud computing, artificial intelligence and data localisation requirements. Listed REITs provide an efficient way for investors to gain exposure to stabilised facilities, with Singapore and Japan acting as core hubs and Southeast Asia featuring more prominently in acquisition strategies.

Healthcare assets form the second major shift. In Japan, ageing demographics continue to drive demand for hospitals and senior care facilities. In Singapore, strict regulation and high barriers to entry enhance income visibility. While returns in healthcare tend to be lower than in more cyclical sectors, income stability has become increasingly attractive.

Logistics assets have also grown in importance. Supported by e-commerce growth and regional trade flows, modern logistics facilities benefit from high occupancy and specifications that support consistent distributions.

Daily Trading Draws Investors Back

Liquidity defines this phase of the REIT cycle. With private real estate transaction volumes subdued and price discovery challenging, REITs offer daily trading, transparent valuation and regulatory oversight. Institutional investors have returned to listed property as a practical route to real estate exposure without extended lock-in periods.

For retail investors in Japan, Singapore and the Philippines, the appeal lies in income, accessibility and governance. By early 2026, yield spreads over government bonds had stabilised at levels that supported renewed allocations.

The renewed strength of Asian REITs reflects more than a cyclical rebound. It points to a sector that has diversified its assets, strengthened balance sheets and adapted to new economic conditions. With liquidity improving and portfolio quality evolving, REITs remain a significant force in how real estate capital moves across Asia.

![[IRHM] logo](https://irhmagazine.com/wp-content/uploads/2025/08/IRHM-AWARDS-2025-1024x683.jpg)