The global luxury property market is shifting. As 2026 begins, high-end homes are no longer judged only by their location or the quality of their finishes. Instead, they are increasingly seen as an extension of personal taste and lifestyle, much like a watch, a car or a hotel brand. This change has driven growing interest in branded residences, homes developed with luxury brands.

Branded residences linked to hotels such as Four Seasons and Ritz-Carlton have existed for many years. What’s changed is the pace at which brands from outside hospitality have entered the market. Buyers can now choose towers associated with automotive names such as Bugatti or Mercedes-Benz, or homes influenced by fashion houses like Armani or Bulgari. This trend is particularly visible in two very different markets: Dubai and Phuket. Despite their contrasting settings, both show that buyers are prepared to pay a clear premium for a brand they recognise and trust.

From road and runway to real estate

For car manufacturers and fashion houses, the move into residential property is largely about extending their brand into everyday living. Buyers who are loyal to a particular car or fashion label often expect similar design standards and service levels in their homes. Property offers a way for brands to translate these values into a long-term, physical setting.

There is also a commercial reason behind this expansion. Automotive brands are adapting to new technologies and regulatory pressures, while fashion houses face increasingly competitive global markets. Real estate provides a longer-term revenue stream and helps brands diversify. For buyers, the attraction lies in reassurance. In a volatile global environment, a recognised brand offers a sense of consistency, particularly when it comes to building quality, maintenance and ongoing management.

How the premiums stack up

The so-called brand premium refers to the additional amount buyers are willing to pay for a branded home compared with a similar non-branded property. Market data from 2025 and early 2026 shows that this premium remains firmly in place in both Dubai and Phuket, though it varies by location and project.

Dubai: a mature branded market

Dubai is seen as one of the most developed markets for branded residences. According to CBRE’s UAE Branded Residence Report 2025, released in December, branded homes in Dubai commanded an average premium of 64% over non-branded properties in the first half of 2025, significantly above the global average of around 30%. The full-year 2025 average premium across comparable locations was 43%.

In 2025, Dubai recorded 12,873 branded residence transactions, up 2.1% year-on-year, with total sales value rising 38% to AED 79.1 billion ($21.36 billion) from AED 57.3 billion in 2024. This divergence between volume and value highlights a clear shift towards larger-ticket transactions and increased capital concentration at the top end of the market.

The average price per square foot for branded residences reached AED 3,777 ($1,028) in 2025, representing a 15% increase from 2024’s AED 3,288. Branded residences continued to command a significant premium over non-branded residential stock, averaging approximately 43% across comparable locations throughout 2025, though in the first half of the year this premium stood at 64% in prime locations.

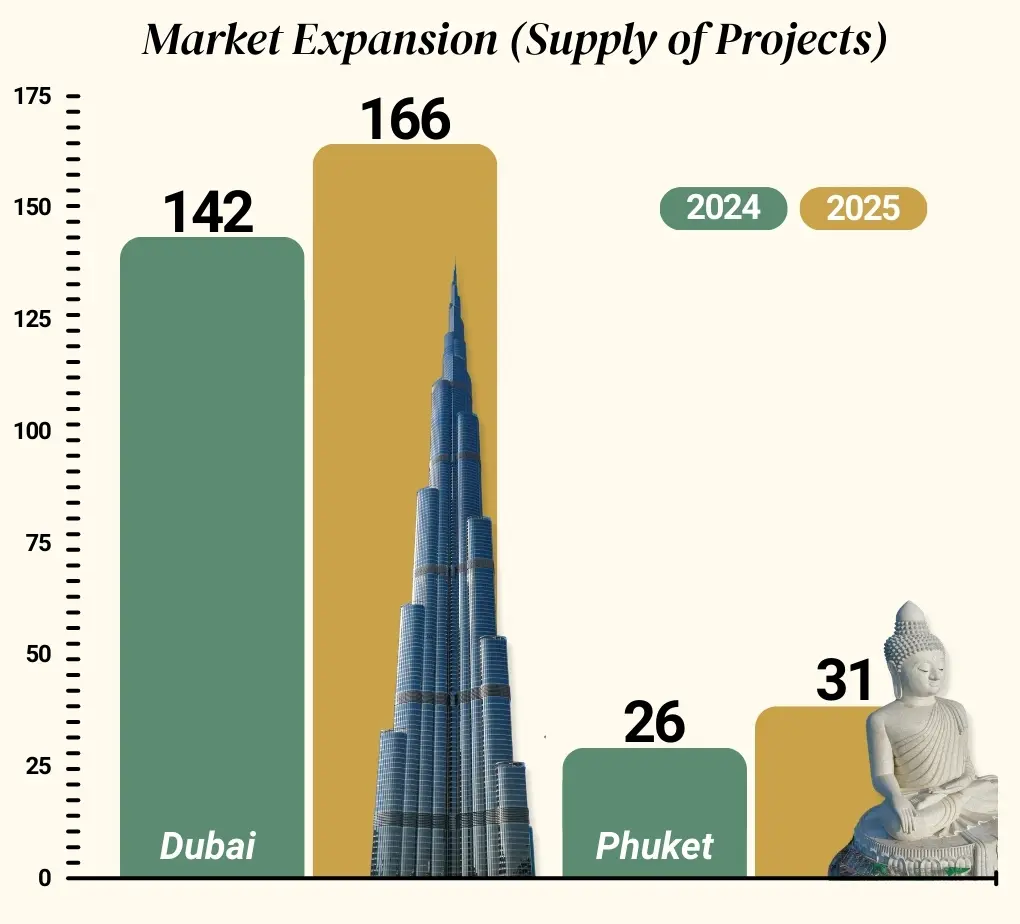

High-profile developments have helped shape this segment. These include Bugatti Residences in Business Bay, Armani Beach Residences on Palm Jumeirah, Mercedes-Benz Places in Downtown Dubai and the Bulgari Lighthouse on Jumeirah Bay Island. By the end of 2025, Dubai had 166 branded residence projects with 51,692 units, comprising approximately 18,842 ready units and 32,850 units under construction. Aman Hotels & Resorts made its Dubai debut in 2025, instantly becoming one of the most premium branded properties with average prices reaching AED 17,328 per square foot, though select trophy units at Atlantis The Royal transacted as high as AED 18,294 per square foot.

Branded residences now account for 13% of Dubai’s residential sales value and 5.8% of transaction volume. More than 80% of branded transactions remain off-plan, reflecting investor appetite for early access to flagship developments. According to Dubai-based real estate consultancy VVS Estate, the market is projected to grow by 80% by 2030, reaching approximately 250 branded developments across the emirate.

Downtown Dubai leads with 22 branded projects, followed by Business Bay with 17 and Palm Jumeirah with 16. Off-plan transactions dominated activity in 2025, accounting for approximately 82% of annual branded residence transactions.

Phuket: a resort-led alternative

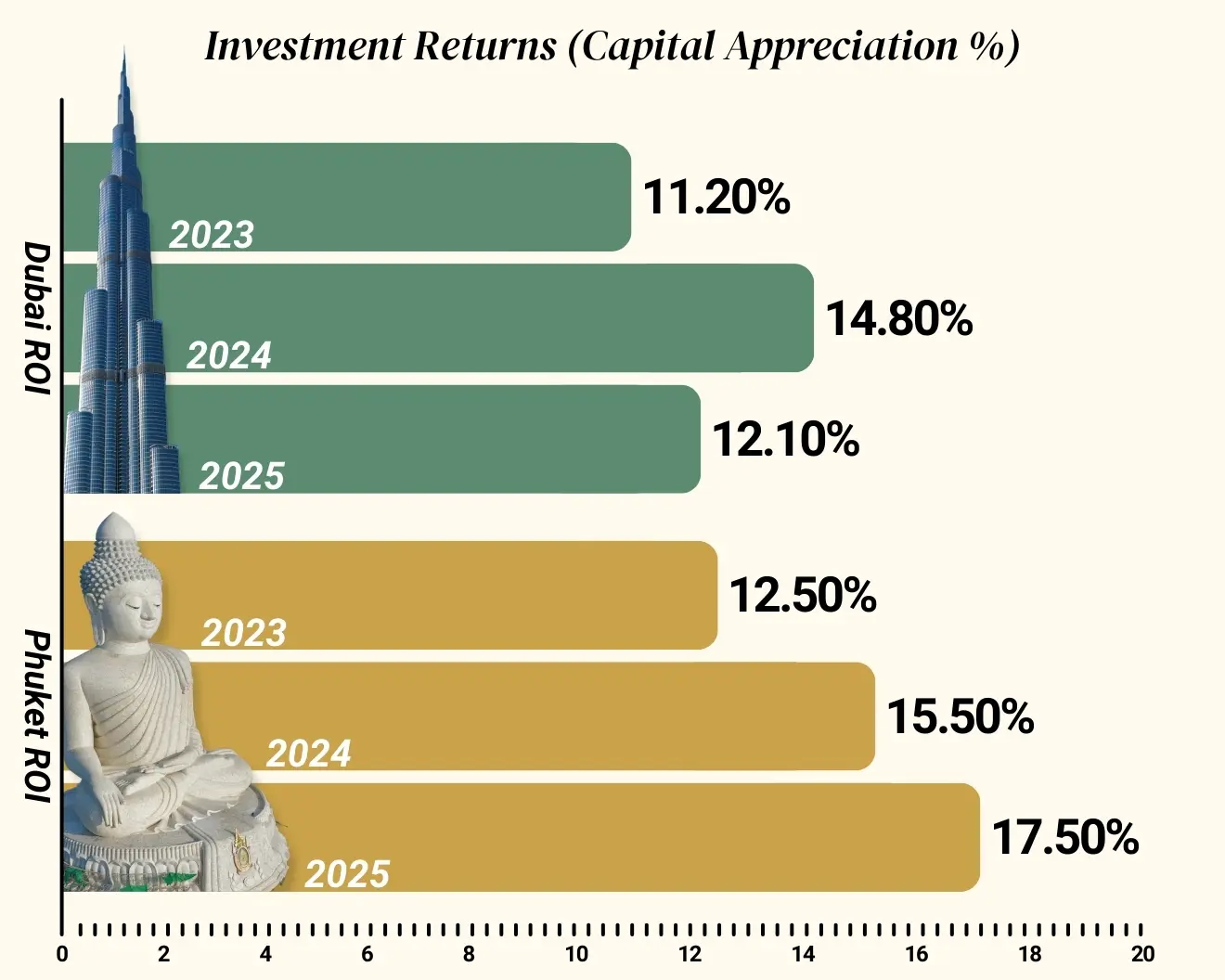

Phuket offers a contrasting model of branded living. Known primarily as a resort destination, the island has seen branded residences emerge as a key part of its luxury property market. Branded residences are commanding extraordinary premiums, with properties in the premium branded segment achieving 15 to 20% annual appreciation in 2025, significantly outpacing the overall market’s 10 to 15% growth.

Examples include Banyan Tree Residences at Laguna Phuket, the Residences at InterContinental Phuket Resort on Kamala Beach, Twinpalms Residences MontAzure and The Standard Residences in Bang Tao. These developments typically combine private ownership with resort-style services, appealing to buyers looking for both lifestyle use and rental income.

Investment analysts tracking the Phuket market note that branded residences in high-demand locations show potential returns of 12 to 18% in capital appreciation, supplemented by average net rental yields of 5 to 7% after management fees. Well-managed branded properties achieve gross rental yields of 6 to 8%, with properties in northern beach areas like Bang Tao and Cherngtalay increasingly matching the 8 to 10% yields traditionally associated with Patong as investor focus shifts northward.

The January 2026 launch of ETRO Residences at Gardens of Eden in Bang Tao set an island record at THB 830,000 per square metre ($26,350), more than four times Phuket’s branded residence average, with 25% of units sold within three days. This “ETRO Effect” further demonstrates the premium positioning of Bang Tao’s luxury branded segment.

The branded residence market in Phuket has surged to a value exceeding THB 80 billion, signalling a major shift in luxury asset investment. The median condominium price now stands at THB 144,000 per square metre (approximately $4,000), while villas average THB 70,000 per square metre.

Lock-up-and-leave living

A significant factor supporting demand in 2026 is the growing preference for a lock-up-and-leave lifestyle. Many high-net-worth individuals now divide their time between several countries each year and want homes that do not require constant oversight.

Branded residences are designed to meet this need. Professional management teams handle security, maintenance, landscaping and housekeeping, allowing owners to travel freely. In Phuket, this model is particularly attractive as approximately 60 to 70% of purchases are made by foreign nationals, primarily using cash due to limited access to local mortgages from Thai banks.

Foreign buyers can own freehold condominium units (up to 49% of units in any building) but cannot directly own land. For villas, foreigners typically use a secure 30-year leasehold structure, which is protected by Thai law. The relatively low level of debt in the market adds to its appeal for long-term investors.

In Dubai, the tax-free environment (though buyers pay a standard 4% Dubai Land Department transfer fee on transactions, which some developers absorb as a promotional incentive) and safe-haven status attract high-net-worth individuals from Europe, India, Russia and the GCC. Phuket sees demand primarily from Russia, China and India, with additional interest from European buyers (particularly Germany and the UK), Australia and Kazakhstan.

Is the premium justified?

Some observers question whether the higher prices attached to branded residences can be maintained over time, particularly in markets where premiums exceed 60%. The market is maturing fast, and buyers are becoming more selective.

According to CBRE’s UAE Branded Residence Report 2025, the sector has transitioned from a niche offering to a defining feature of the UAE’s luxury real estate market over the past five years, driven by global wealth migration and strong demand for quality and security.

However, performance to date shows that other factors are equally important. Limited supply, consistent management standards and international demand have helped many branded properties hold their value during slower market periods. As more brands enter the sector, successful projects increasingly need to offer tangible benefits such as wellness facilities, concierge-led services, privacy features and clearly defined service levels.

The rise of branded residences is closely linked to wealth migration trends. The UAE’s GDP growth forecast for 2025 was revised up to 5.3%, supported by non-oil sector expansion and continued inflows of high-net-worth individuals. Phuket recorded over 3.8 million visitors in Q1 2025 alone, with tourism revenue reaching THB 149 billion for that quarter.

Higher service fees remain a consideration. While branded properties offer professional management, owners pay for these services through higher monthly fees compared to non-branded alternatives. In some cases, these can be 30 to 50% higher than conventional luxury properties.

What comes next

The comparison between Dubai and Phuket shows that branded residences are no longer a niche offering. In Dubai, the premium is closely linked to status, design and urban living. In Phuket, it reflects ease of ownership and a resort-based lifestyle.

In both markets, demand is driven by an international audience that places a high value on reliability, time efficiency and professional management. As 2026 unfolds, the divide between branded and non-branded luxury homes is likely to remain a defining feature of the global high-end residential market.

With Savills projecting the branded residences sector to hit 910 schemes globally by end of 2025 (up 19% from 764 in December 2024), and an additional 837 contracted projects scheduled through 2032, the sector shows no signs of slowing. The Middle East and North Africa region has exploded 187% in five years, led by Dubai and the Gulf states, while Asia Pacific has grown 55%, driven by Vietnam, Thailand and India.

Whether this growth proves sustainable will depend on developers maintaining quality standards and delivering the professional management that justifies the premium. For now, buyers seem willing to pay for the reassurance a recognised brand provides.

![[IRHM] logo](https://irhmagazine.com/wp-content/uploads/2025/08/IRHM-AWARDS-2025-1024x683.jpg.webp)