Terms of Reference

PaaS (Property-as-a-Service): A transition from selling physical space to providing a bundled, subscription-based experience that includes housing/office space, utilities, and lifestyle services.

Brown Discount: The reduction in market value (averaging 20% in 2026) applied to older, non-integrated, or carbon-intensive buildings that do not meet modern ESG or tech standards.

Operational Alpha: The additional profit or yield generated through superior technology-driven management (like AI energy grids) rather than just market appreciation.

IoE (Internet of Everything): The deep integration of data, processes, people, and physical sensors into a building’s core foundation to enable real-time responsive environments.

Fractional Ecosystems: An investment model where high-value, tech-integrated developments are split into digital tokens, allowing for smaller investment entries and higher market liquidity.

Hyper-Proximate District: An evolution of the 15-minute city, where all essential lifestyle, health, and workspace needs are accessible within a 100-metre radius of a residential hub.

The real estate mantra has officially shifted. While location remains a cornerstone, the industry’s new pulse is defined by a different metric: Integration. We are no longer simply in the business of selling or leasing four walls; we are in the era of Property-as-a-Service (PaaS).

The Narrative: From Shelter to Service

Stepping into a modern ‘Hub’ in London or Manchester feels less like entering a building and more like joining a platform. Your apartment doesn’t just house you; it sustains you. The walls are embedded with AI-managed energy grids that optimise consumption in real-time, while communal floors serve as fluid spaces, shifting from high-octane co-working zones by day to wellness-centric lounges by night.

This is the ‘Ecosystem’ model. Standalone office blocks and isolated residential towers are rapidly becoming ‘stranded assets’. The winners in today’s market are developments that function as self-sustaining organisms, blending living, working, and localised production under one roof.

The Global Landscape: Strategic Benchmarks

Across the UK and Europe, the focus has pivoted toward Operational Real Estate (OPRE). Investors are moving away from passive shells and toward buildings that host active, tech-enabled businesses.

- In the UK: Institutional capital is flooding into Build-to-Rent (BTR) communities that prioritise ‘access over ownership’. These developments offer a digital-first lifestyle, where maintenance, utilities, and lifestyle perks are bundled into a single monthly subscription.

- The Middle East: Giga-projects in the region have moved past the conceptual phase. These ‘Lifestyle Communities’ are setting global standards for Invisible Sustainability, utilising carbon-neutral materials and automated waste-to-energy systems that operate entirely out of sight.

- Asia-Pacific: High-density hubs in Singapore and Tokyo are tackling demographic shifts through Multi-Generational Ecosystems. These projects integrate luxury independent living for seniors with tech-ready studios for young professionals, creating a symbiotic social loop that fosters community.

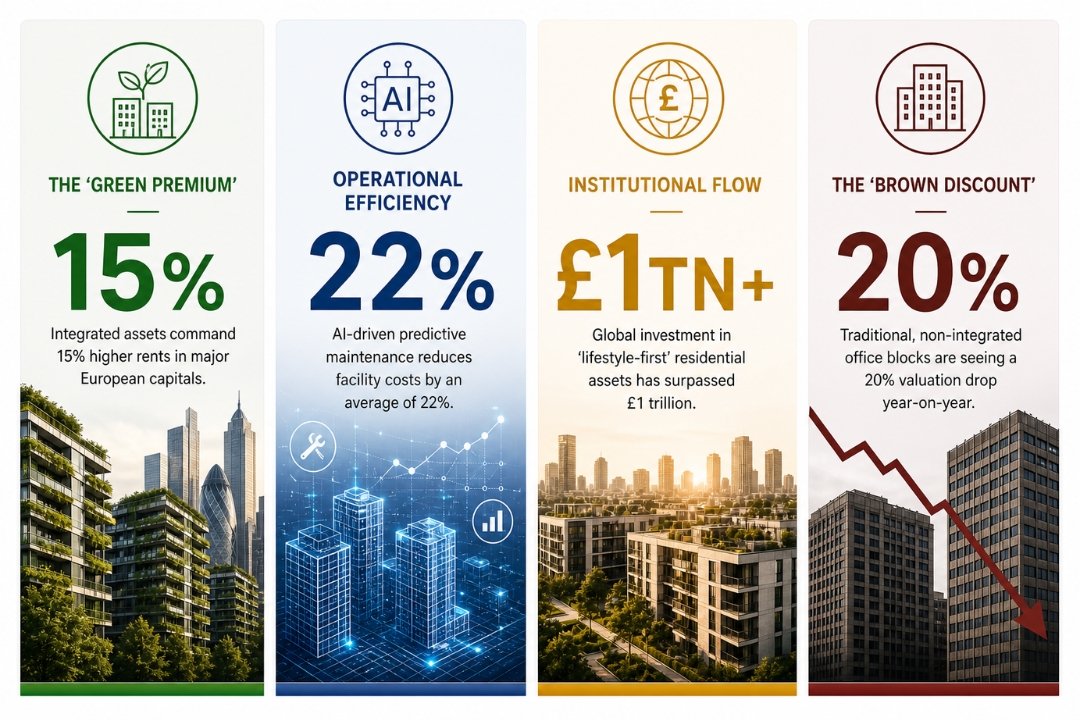

By The Numbers: The Quantified Market

The transition towards integrated, lifestyle-led real estate is not speculative, it is being decisively priced in. Market data now clearly demonstrates the superior performance, operational efficiency and capital inflows driving this new asset class:

Technology & Innovation: The Digital Backbone

Digital transformation is no longer about having a fast Wi-Fi connection. It’s about the Internet of Everything (IoE) being baked into the foundation.

- Predictive Operations: Property managers no longer wait for a system to fail. Sensors predict equipment fatigue weeks in advance, ensuring zero downtime for residents and tenants.

- Adaptive Materials: From ‘Smart Glass’ that adjusts transparency based on the sun’s angle to low-carbon timber constructions, the buildings themselves are becoming active participants in carbon reduction.

- Tokenised Ownership: Blockchain platforms are democratising the market, allowing smaller investors to own fractional shares in high-yield ecosystems, significantly increasing market liquidity.

Prominent Blueprints

Whilst several flagship projects have recently come online, three stand out as the current gold standard:

The Battersea Evolution (UK): Representing the latest phase of the Battersea Power Station redevelopment, this is a masterclass in the ‘15-minute neighbourhood’ taken a step further. High end ecosystem living is defined here by ultra local access, with residents able to reach bespoke healthcare, EV fleet sharing, and essential services within a 100 metre radius, setting a new benchmark for integrated urban convenience in London.

The Wood City Hub (Sweden): Anchored in Stockholm’s landmark Stockholm Wood City, this project represents the pinnacle of mass timber construction. By 2026, it has effectively de-risked the concept for global developers, proving that large scale urban ecosystems can be delivered entirely through renewable materials without compromising on structural integrity or modern luxury standards.

The Dubai Waterfront Modules: Aligned with the ambitions of the Dubai 2040 Urban Master Plan, this is a technology led ecosystem where AI governs daily living. From optimising indoor climate conditions to managing on site vertical farming for local produce, the development reflects a growing regional focus on food security, efficiency, and fully integrated smart districts.

Conclusion: The New Asset Class

The implication for developers, investors, and operators is clear. Real estate is no longer being evaluated purely on location, design, or even sustainability in isolation. It is being judged on its ability to function as a living, responsive ecosystem.

The building is no longer the product; the experience within it is. Assets that fail to engage with their occupants and evolve through data are not simply falling behind, they are being systematically repriced by the market.

What is emerging is not an incremental shift, but the formation of an entirely new asset class. One that blends infrastructure, technology, hospitality, and community into a single, integrated proposition. In this model, value is no longer static, it is continuously generated through service, adaptability, and user engagement.

For those willing to embrace this transition, the opportunity is significant. For those who do not, the risk is equally clear. In the age of ecosystems, a building that does not integrate is no longer competing, it is quietly becoming irrelevant.

Key Takeaways

- Metric Shift: Valuation is moving from “rent per sq ft” toward User Lifetime Value (LTV).

- The 15% Premium: Integrated “Ecosystem” assets command a 15% rental premium in major capitals.

- Stranded Risk: Non-integrated assets are seeing a 20% YoY valuation drop.

- Operational Alpha: AI-driven predictive systems reduce facility costs by an average of 22%.

- Global Maturity: Flagship projects like Battersea and Wood City have successfully de-risked the model for institutional capital.

![[IRHM] logo](https://irhmagazine.com/wp-content/uploads/2025/08/IRHM-AWARDS-2025-1024x683.jpg)